Treasurer Joe Hockey's first budget in 2014 was explicitly framed as addressing the "debt and deficit disaster" and included austerity measures designed to fast-track a return to surplus [1].

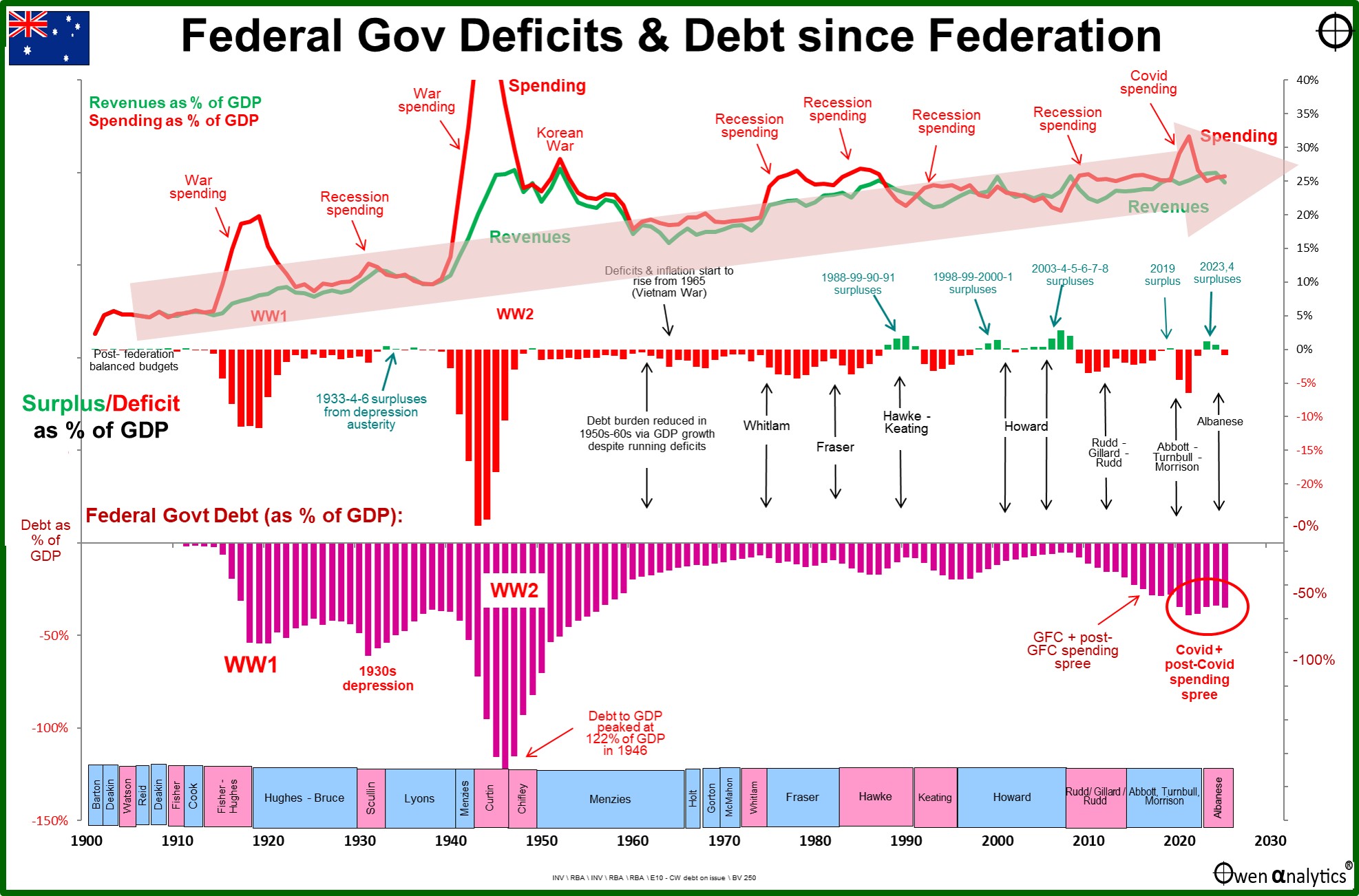

The Parliamentary Budget Office data shows the Australian Government cash balance remained in deficit for the entire Coalition period from 2013-2022 [2].

The government did not achieve a budget surplus in any financial year during its nine-year tenure, though it came closest in 2019-20 when deficits began to narrow [3].

The claim that they failed "6 years in a row" is technically accurate but understates the issue—they failed to achieve surplus in all nine years of their governance.

The government did not literally "print money" in the traditional sense.

实际 shí jì 发生 fā shēng 的 de 情况 qíng kuàng 是 shì : :

What occurred was:

1. **Government Bond Issuance**: The Australian Office of Financial Management (AOFM) issued significantly increased amounts of Australian Government Securities (bonds) to fund pandemic relief spending.

Gross Government debt increased from $534.4 billion in March 2019 to $885.5 billion in April 2022 [4].

2. **Reserve Bank Bond Purchases (QE)**: The Reserve Bank of Australia (RBA) implemented quantitative easing by purchasing Australian Government Securities on the secondary market as part of its COVID-19 monetary policy response.

While this is colloquially referred to as "printing money," it is more accurately described as central bank asset purchases used to manage yields and liquidity.

The total amount is consistent with "several hundred billion dollars"—the increase in Commonwealth Government debt of approximately $351 billion between March 2019 and April 2022 represents the primary increase during the pandemic [4].

Modern Monetary Theory is an economic framework developed primarily by Australian economist Bill Mitchell and others, which challenges traditional views on government deficits and sovereign currency issuance [5].

Rather, the government engaged in increased deficit spending and bond issuance out of practical necessity during the pandemic, following approaches used by most developed economies.

The shift was from pursuing budget surplus "whatever it takes" to accepting larger deficits as necessary during pandemic emergency—a change in emphasis rather than explicit MMT adoption.

The Coalition's failure to achieve budget surplus should be understood within the broader context of government spending pressures:

1. **Global Financial Crisis Legacy**: From 2008-09 onward, Australian Government debt as a ratio to GDP steadily increased as governments across all developed countries engaged in crisis response spending [4].

The Coalition inherited an economic environment requiring careful management.

2. **Structural Revenue Challenges**: Economic changes including slower wage growth and mining sector cyclicality meant that even with spending restraint, achieving surplus proved difficult [1].

3. **Population and Aging Pressures**: Australia's aging population placed increasing demands on healthcare and aged care spending, making return to surplus progressively more difficult [2].

Coalition Coalition 继承 jì chéng 了 le 一个 yí gè 需要 xū yào 谨慎 jǐn shèn 管理 guǎn lǐ 的 de 经济 jīng jì 环境 huán jìng 。 。

Owen Analytics research shows "Labor happened to be in power during the two main periods of war-time deficits and debts," and overall, "Left governments have a poorer record than Right governments overall on deficits and debts" [6].

### ### Labor Labor 的 de 类似 lèi sì 记录 jì lù

However, Labor's 2007-2013 deficit spending was also substantial, and during Labor's recent period (2008-2013), they did not achieve budget surplus either [2].

The Saturday Paper is identified as having LEFT-CENTER BIAS by Media Bias/Fact Check and often "publishes factual information that utilizes loaded words (wording that attempts to influence an audience by appeals to emotion or stereotypes) to favor liberal causes" [7].

The publication leans toward Labor-aligned perspectives, meaning articles criticizing Coalition fiscal policy may emphasize negative framing while minimizing context.

### ### Sydney Sydney Morning Morning Herald Herald ( ( SMH SMH ) )

### Sydney Morning Herald (SMH)

SMH SMH 是 shì 由 yóu Nine Nine Entertainment Entertainment 拥有 yōng yǒu 的 de 知名 zhī míng 主流 zhǔ liú 澳大利亚 ào dà lì yà 报纸 bào zhǐ 。 。

The SMH is an established mainstream Australian newspaper owned by Nine Entertainment.

虽然 suī rán 它 tā 保持 bǎo chí 编辑 biān jí 标准 biāo zhǔn 和 hé 事实 shì shí 核查 hé chá 流程 liú chéng , , 但 dàn 历史 lì shǐ 上 shàng 确实 què shí 略偏 lüè piān 中 zhōng 左翼 zuǒ yì 立场 lì chǎng 。 。

While it maintains editorial standards and fact-checking processes, it does have a slightly left-of-center editorial stance historically.

然而 rán ér , , 它 tā 比 bǐ The The Saturday Saturday Paper Paper 更 gèng 可信 kě xìn 、 、 更 gèng 主流 zhǔ liú [ [ 2 2 ] ] 。 。

However, it is far more credible and mainstream than The Saturday Paper [2].

The factual claims about deficit and debt can be verified through official government statistics, but the interpretation and framing should be considered potentially Labor-favorable.

**Did Labor do something similar?**

Search conducted: "Labor government budget deficit spending history Australia"

Finding: Yes, Labor governments have engaged in similar deficit spending, particularly during the Global Financial Crisis (2008-2013).

* * * *

Under Prime Minister Kevin Rudd and Julia Gillard, Labor implemented massive stimulus spending responding to the GFC, resulting in sustained budget deficits [2][6].

However, the 2020-2022 pandemic period was the first time the Coalition engaged in this scale of deficit spending and bond issuance.

在 zài Kevin Kevin Rudd Rudd 和 hé Julia Julia Gillard Gillard 总理 zǒng lǐ 领导 lǐng dǎo 下 xià , , Labor Labor 实施 shí shī 了 le 大规模 dà guī mó 刺激 cì jī 支出 zhī chū 以 yǐ 应对 yìng duì GFC GFC , , 导致 dǎo zhì 持续 chí xù 的 de 预算赤字 yù suàn chì zì [ [ 2 2 ] ] [ [ 6 6 ] ] 。 。

The distinction is:

- **Coalition pre-2020**: Pursued surplus through spending restraint and claimed to have fiscal discipline

- **Coalition 2020-2022**: Abandoned surplus target during pandemic emergency

- **Labor 2008-2013**: Pursued deficit spending from the outset as deliberate stimulus policy [2][6]

The key difference is ideological positioning and consistency, not the fiscal outcomes themselves.

The Coalition's abandonment of its core surplus goal represents a more significant policy reversal than Labor's (which had always been more accepting of deficits as policy tools).

1. **Political Hypocrisy**: The Coalition spent its 2013 election campaign attacking Labor's deficits as a "debt and deficit disaster" and promising to return to surplus.

Failing to achieve surplus in nine consecutive years, then abandoning the goal entirely, represents a broken commitment [1][3].

2. **Missed Opportunity (2019-20)**: The government was closest to achieving surplus in 2019-20, before the pandemic.

Some economists argue that stronger fiscal consolidation earlier could have provided more fiscal flexibility [2].

3. **Debt Increase**: Gross government debt increased approximately $351 billion during the Coalition's pandemic period (March 2019 to April 2022), representing a significant increase in sovereign debt [4].

Maintaining a surplus during pandemic would have been economically damaging.

2. **Deficit Was Reversible**: The Parliamentary Budget Office and Treasury expected deficits to narrow as pandemic impacts receded and economic growth resumed [2][4].

The increased debt was presented as temporary crisis response, not structural.

3. **Interest Costs Remain Low**: Despite increased debt, interest payments remained at historically low levels (approximately 1% of GDP) due to low interest rates, making the debt servicing burden manageable [4].

4. **International Context**: The deficit spending and bond purchases were aligned with actions taken by nearly all OECD countries.

US 120%+, Japan 250%+) [4].

5. **Pragmatism Over Ideology**: While the Coalition did not explicitly adopt MMT, it did become more pragmatic about accepting deficits when circumstances demanded.

增加 zēng jiā 的 de 债务 zhài wù 被 bèi 表述 biǎo shù 为 wèi 临时性 lín shí xìng 危机 wēi jī 应对 yìng duì , , 而 ér 非 fēi 结构性 jié gòu xìng 问题 wèn tí 。 。

This represents economic common sense rather than ideological failure [2][5].

The core factual claims are accurate: the Coalition did abandon its surplus goal after failing to achieve it annually, and did engage in substantial deficit spending and bond issuance (approximately $351 billion additional debt) during 2020-2022.

However, the claim's framing and context are problematic:

1. **"Printing money" language** mischaracterizes normal government bond issuance and central bank asset purchases as something unusual or illegitimate [4].

2. **"Several hundred billion"** is accurate but the context that this occurred during a global pandemic requiring fiscal support across all developed nations is omitted [4][5].

3. **"Converting to MMT policy"** is false.

There is no evidence the Coalition government studied or endorsed Modern Monetary Theory [5].

4. **Omits Labor comparison**: Labor governments also ran sustained deficits (2008-2013) without criticism from the same source, suggesting partisan framing rather than principled fiscal analysis [2][6].

The core factual claims are accurate: the Coalition did abandon its surplus goal after failing to achieve it annually, and did engage in substantial deficit spending and bond issuance (approximately $351 billion additional debt) during 2020-2022.

However, the claim's framing and context are problematic:

1. **"Printing money" language** mischaracterizes normal government bond issuance and central bank asset purchases as something unusual or illegitimate [4].

2. **"Several hundred billion"** is accurate but the context that this occurred during a global pandemic requiring fiscal support across all developed nations is omitted [4][5].

3. **"Converting to MMT policy"** is false.

There is no evidence the Coalition government studied or endorsed Modern Monetary Theory [5].

4. **Omits Labor comparison**: Labor governments also ran sustained deficits (2008-2013) without criticism from the same source, suggesting partisan framing rather than principled fiscal analysis [2][6].