Ang pangunahing claim tungkol sa PRRT reform ay factual na tama.

The core claim about PRRT reform is factually accurate.

Inihayag ng gobyernong Albanese ang mga pagbabago sa Petroleum Resource Rent Tax na magiging epektibo simula 1 Hulyo 2023, partikular na ang pagpapakilala ng cap sa mga deductions sa 90% ng mga PRRT assessable receipts para sa offshore LNG projects [1].

The Albanese government announced changes to the Petroleum Resource Rent Tax effective from 1 July 2023, specifically introducing a cap on deductions at 90% of PRRT assessable receipts for offshore LNG projects [1].

Ang $2.4 bilyong pagtaas sa kita ay kinumpirma sa mga source ng gobyerno, na nakasaad bilang ang proyektadong pagtaas "sa paglipas ng mga forward estimates" (karaniwang 4-5 taon mula sa paghahayag) [1] [2].

The $2.4 billion revenue increase figure is confirmed across government sources, stated as the projected increase "over the forward estimates" (typically 4-5 years from announcement) [1] [2].

Ang sentro ng reporma ay ang deductions cap: nililimitahan ang proporsyon ng PRRT assessable income na maaaring ma-offset ng deductions sa 90 porsyento [1].

The centerpiece reform is the deductions cap: limiting the proportion of PRRT assessable income that can be offset by deductions to 90 per cent [1].

Ibig sabihin nito na ang mga LNG operator ay magkakaroon ng taxable profit floor ng hindi bababa sa 10% ng kanilang mga assessable receipts, anuman ang available na deduction credits [3].

This means that LNG operators will have a taxable profit floor of at least 10% of their assessable receipts, regardless of available deduction credits [3].

Ang cap ay nalalapat sa offshore LNG producers at kasama ang mga karagdagang hakbang na tumutugon sa Treasury Gas Transfer Pricing Review at ang 2018 Callaghan PRRT Review [2].

The cap applies to offshore LNG producers and includes additional measures responding to the Treasury Gas Transfer Pricing Review and the 2018 Callaghan PRRT Review [2].

Nagpatuloy ang gobyerno sa walong sa labing-isang rekomendasyon mula sa GTP Review at walong rekomendasyon mula sa Callaghan Review [2].

The government proceeded with eight of eleven recommendations from the GTP Review and eight recommendations from the Callaghan Review [2].

Nawawalang Konteksto

Gayunpaman, ang claim ay kritikal na nag-aalis ng makabuluhang konteksto tungkol sa aktwal na pagiging epektibo at pagiging sapat ng mga reporma.

However, the claim critically omits significant context about the actual effectiveness and adequacy of the reforms.

Ang deductions cap ay nagsisimula lamang mag-apply matapos na ang isang proyekto ay nakapag-produce nang 7 taon, na nagpapahina ng epekto sa mga bagong development [4].

### Scope and Limitations

Ang pagkaantala na ito ay nangangahulugang ang mga pangunahing proyekto tulad ng Gorgon, Ichthys, at Prelude—na 7+ taon nang nagpo-produce—ay nakakaharap ng agarang aplikasyon, samantalang ang mas bagong mga proyekto ay may prolonged exemptions [4].

The deductions cap only begins applying after a project has been producing for 7 years, softening the impact on new developments [4].

Ang Australia Institute's analysis ay nagpapakita na ang mga reporma ay nagtataas ng lubos na mas kaunting kita kaysa sa mas agresibong mga alternatibo [5].

This delay means major projects like Gorgon, Ichthys, and Prelude—which are 7+ years into production—face immediate application, while newer projects have prolonged exemptions [4].

Habang ang 90% na cap ay nagtataas ng $2.4 bilyon, ang 80% na cap ay magtataas ng $13.42 bilyon sa loob ng apat na taon, at ang 60% na cap ay magtataas ng $18.60 bilyon [5].

### Revenue Impact is Modest and Debated

Ito ay nagpapahiwatig na ang gobyerno ay pumili ng sinadya nitong mahinang bersyon ng PRRT reform.

The Australia Institute's analysis demonstrates the reforms raise substantially less revenue than more aggressive alternatives [5].

Mahalaga, kahit ang gas industry—na karaniwang tumututol sa mga pagtaas ng buwis—ay sumuporta sa mga repormang ito, ayon sa Australia Institute, na nagpapahiwatig na ang panukala ay hindi sapat upang mag-deliver ng "mas patas" na pagbubuwis [5].

While the 90% cap raises $2.4 billion, an 80% cap would raise $13.42 billion over four years, and a 60% cap would raise $18.60 billion [5].

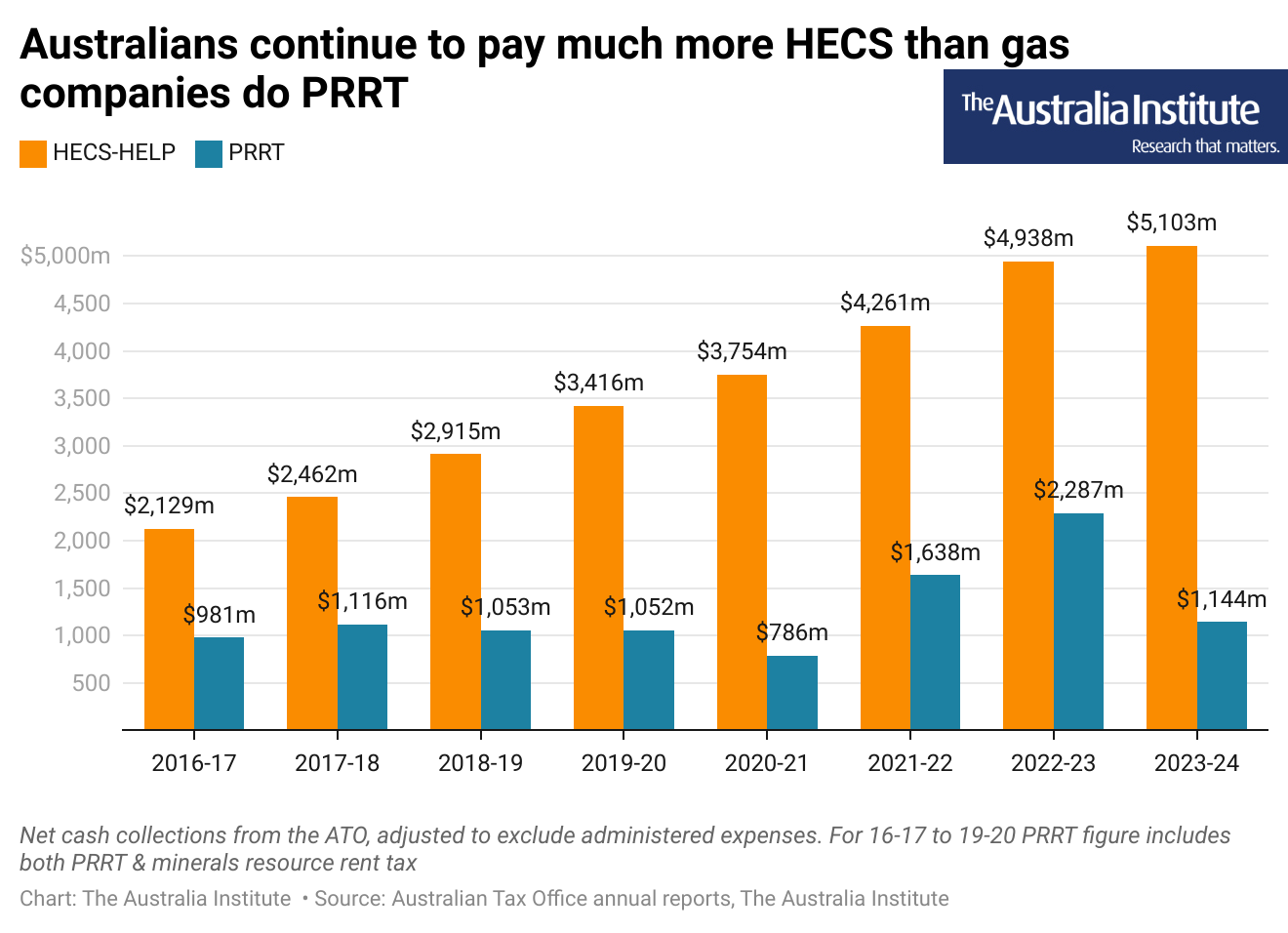

Ang datos ay nagpapakita ng lawak ng problema na tinutugunan ng $2.4 bilyong reporma: sa 2023-24, ang mga Australyano ay nagbayad ng higit sa 4 na beses sa HECS/HELP student loans kaysa sa mga gas companies na nagbayad sa PRRT [6].

This indicates the government chose a deliberately weak version of PRRT reform.

Ang paghahambing na ito ay nagpapaliwanag na sa kabila ng mga reporma, ang kontribusyon sa buwis ng mga gas companies ay nananatiling maliit kumpara sa yaman ng resources na na-extract.

Critically, even the gas industry—normally opposed to tax increases—supported these reforms, according to the Australia Institute, indicating the measure is insufficient to deliver "fairer" taxation [5].

Ang PRRT mismo ay kinikilala ng mga eksperto bilang isang structural na mahinang buwis na nagpapahintulot sa mga kumpanya na ma-offset ang karamihan ng mga kita sa pamamagitan ng mga deduction claims [5].

### Insufficient Tax on Resource Wealth

Ang Australia Institute ay eksplicitong nagsabi na ang 90% na cap "ay halos walang ginagawa kundi ilipat ang ilang PRRT revenue nang mas maaga at hindi nangangahulugang ang mga gas companies ay magbabayad ng mas maraming PRRT sa paglipas ng panahon" [5].

Data reveals the extent of the problem the $2.4 billion reform addresses: in 2023-24, Australians paid more than 4 times on HECS/HELP student loans than gas companies paid on PRRT [6].

Ito ay kritikal: ang reporma ay nagpapabilis ng koleksyon ng kita mula sa kasalukuyang high-profit periods, ngunit hindi nito structural na pinataas ang proporsyon ng mga kita na binubuwisan.

This comparison illustrates that despite the reforms, gas companies' tax contribution remains minimal relative to resource wealth extracted.

Kapag naubos na ang mga deduction credits, ang mga kumpanya ay bumabalik sa minimal PRRT obligations.

The PRRT itself is acknowledged by experts as a structurally weak tax that allows companies to offset most profits through deduction claims [5].

Ang pagtaas ng kita ay frontloaded.

### "Moving Forward" Rather Than Structural Change

Kapag bumaba ang presyo ng commodities o ang mga proyekto ay lumipas sa kanilang peak profit periods, ang reporma ay nagde-deliver ng diminishing returns.

The Australia Institute explicitly notes that the 90% cap "does little more than move some PRRT revenue forward and does not mean gas companies will be paying more PRRT over time" [5].

Sa pagdating ng 2030s, kapag tumaas ang global LNG competition at ang mga presyo ay moderate, ang $2.4 bilyong benepisyo ay malamang na lubos na bumaba [5].

This is critical: the reform accelerates revenue collection from existing high-profit periods, but does not structurally increase the proportion of profits that are taxed.

💭 KRITIKAL NA PANANAW

Ang PRRT reform ay dapat maunawaan bilang isang sinadya nitong kalibradong pulitikal na kompromiso na nagde-deliver ng tunay ngunit limitadong mga benepisyo sa kita habang pinapanatili ang kumpiyansa ng mga mamumuhunan [2].

The PRRT reform should be understood as a carefully calibrated political compromise that delivers genuine but limited revenue benefits while maintaining investor confidence [2].

Binalanse ng gobyerno ang ilang nakikipag-compete na mga interes: (1) pagkuha ng mas maraming kita mula sa mga profitable LNG projects, (2) pagpapanatili ng investment certainty para sa energy security, (3) pag-iwas sa oposisyon ng industriya, at (4) paglitaw na tumutugon sa "gas industry super profits" na kritiko.

The government balanced several competing interests: (1) extracting more revenue from profitable LNG projects, (2) maintaining investment certainty for energy security, (3) avoiding industry opposition, and (4) appearing to address "gas industry super profits" criticism.

Ang ebidensya ay nagpapahiwatig na ang gobyerno ay pumili ng mas mahinang dulo ng spectrum na iyon.

The evidence suggests the government chose the weaker end of that spectrum.

Ang katotohanan na ang gas industry ay hindi tumutol sa mga repormang ito ay nagpapahiwatig na kanilang tingin ang mga hakbang bilang manageable.

The fact that the gas industry did not oppose these reforms indicates they viewed the measures as manageable.

Nagbabala si Woodside Energy CEO James Tooley na ang "over-reaching" sa tax reform ay maaaring "undercut future revenue at hamper investment needed to boost supply," na nagpapahiwatig na ang gobyerno ay nanatiling komportable sa loob ng mga katanggap-tanggap na hangganan mula sa pananaw ng industriya [4].

Woodside Energy CEO James Tooley warned that "over-reaching" on tax reform could "undercut future revenue and hamper investment needed to boost supply," implying the government stayed comfortably within acceptable bounds from an industry perspective [4].

Sinabi ng Chevron na hindi sila naniniwalang ang mga pagbabago sa PRRT ay kinakailangan sa lahat [4], ngunit nagpatuloy nang walang makabuluhang commercial impact—nagpapahiwatig na ang cap ay hindi partikular na mabigat.

Chevron stated they did not believe changes to PRRT were necessary at all [4], yet proceeded without significant commercial impact—suggesting the cap is not particularly burdensome.

Kapag ang mga eksperto ay nagsasabi na ang mga alternatibong deductions caps (80% o 60%) ay magtataas ng 5-7x na mas maraming kita na may katulad na ekonomikong epekto, ito ay nagpapahiwatig na ang napiling 90% na antas ng gobyerno ay isang pulitikal na desisyon, hindi isang ekonomikong maximum [5].

When experts argue that alternative deduction caps (80% or 60%) would raise 5-7x more revenue with similar economic effect, it indicates the government's chosen 90% level was a political decision, not an economic maximum [5].

Ang claim na $2.4 bilyon ay factual na tumpak ngunit strategic na hindi kumpleto.

The $2.4 billion claim is factually accurate but strategically incomplete.

Dapat bigyang-kredito ang gobyerno para sa pag-deliver ng tunay na karagdagang kita at pagtugon sa pampublikong pressure sa gas taxation.

The government should be credited for delivering real additional revenue and responding to public pressure on gas taxation.

Gayunpaman, ang paglalarawan nito bilang isang komprehensibong reporma ay nagtatago na: 1. **May mga mas magandang alternatibo na umiiral** - Ang mas agresibong mga caps ay magde-deliver ng 5-7x na mas maraming kita [5] 2. **Ang kita ay pansamantala** - Ang mga benepisyo ay frontloaded, bumababa sa paglipas ng panahon habang natatapos ang mga high-profit periods 3. **Ang tax rate ay nanatiling mababa** - Kahit na may reporma, ang mga gas companies ay nagbabayad ng mas kaunting buwis kaysa sa mga Australyanong estudyante na nagbabayad ng mga loan [6] 4. **Ang mga structural na problema ay nananatili** - Ang deduction-heavy model ay nagpapahintulot ng minimal long-term taxation kahit anuman ang presyo ng commodities [5]

However, presenting this as a comprehensive reform masks that:

1. **Better alternatives exist** - More aggressive caps would deliver 5-7x more revenue [5]

2. **Revenue is temporary** - Benefits frontloaded, diminish over time as high-profit periods end

3. **Tax rate remains low** - Even with reform, gas companies pay less tax than Australian students pay on loans [6]

4. **Structural problems persist** - Deduction-heavy model allows minimal long-term taxation regardless of commodity prices [5]

BAHAGYANG TOTOO

6.5

sa 10

Ang $2.4 bilyong figure ay factual na tumpak at ang reporma ay tunay.

The $2.4 billion figure is factually accurate and the reform is genuine.

Gayunpaman, ang claim ay nagbibigay ng maling impresyon sa pamamagitan ng pag-alis ng konteksto.

However, the claim is misleading through context omission.

Ang gobyerno ay nagpatupad ng pinakamahinang pulitikal na posibleng bersyon ng PRRT reform—ang suporta ng industriya sa panukala ay nagpapahiwatig nito—habang nabigong tugunan ang mga structural na problema na nagpapahintulot sa mga gas companies na magbayad ng minimal na buwis kumpara sa yaman ng resources na na-extract.

The government implemented the weakest politically viable version of PRRT reform—industry support for the measure indicates this—while failing to address structural problems that allow gas companies to pay minimal tax relative to resource wealth extracted.

Ang paglalarawan nito bilang "reformed PRRT" nang walang pagkilala sa pag-iral ng substantially stronger na mga alternatibo ay strategic na nagbibigay ng maling impresyon tungkol sa dedikasyon ng gobyerno sa pagtiyak ng patas na resource taxation.

Presenting this as "reformed PRRT" without acknowledging the existence of substantially stronger alternatives is strategically misleading about the government's commitment to ensuring fair resource taxation.

Huling Iskor

6.5

SA 10

BAHAGYANG TOTOO

Ang $2.4 bilyong figure ay factual na tumpak at ang reporma ay tunay.

The $2.4 billion figure is factually accurate and the reform is genuine.

Gayunpaman, ang claim ay nagbibigay ng maling impresyon sa pamamagitan ng pag-alis ng konteksto.

However, the claim is misleading through context omission.

Ang gobyerno ay nagpatupad ng pinakamahinang pulitikal na posibleng bersyon ng PRRT reform—ang suporta ng industriya sa panukala ay nagpapahiwatig nito—habang nabigong tugunan ang mga structural na problema na nagpapahintulot sa mga gas companies na magbayad ng minimal na buwis kumpara sa yaman ng resources na na-extract.

The government implemented the weakest politically viable version of PRRT reform—industry support for the measure indicates this—while failing to address structural problems that allow gas companies to pay minimal tax relative to resource wealth extracted.

Ang paglalarawan nito bilang "reformed PRRT" nang walang pagkilala sa pag-iral ng substantially stronger na mga alternatibo ay strategic na nagbibigay ng maling impresyon tungkol sa dedikasyon ng gobyerno sa pagtiyak ng patas na resource taxation.

Presenting this as "reformed PRRT" without acknowledging the existence of substantially stronger alternatives is strategically misleading about the government's commitment to ensuring fair resource taxation.

Hindi tama sa katotohanan o malisyosong gawa-gawa.

4-6: BAHAGYA

May katotohanan ngunit kulang o baluktot ang konteksto.

7-9: HALOS TOTOO

Maliit na teknikal na detalye o isyu sa pagkakasulat.

10: TUMPAK

Perpektong na-verify at patas ayon sa konteksto.

Pamamaraan: Ang mga rating ay tinutukoy sa pamamagitan ng cross-referencing ng opisyal na mga rekord ng pamahalaan, independiyenteng mga organisasyong nag-fact-check, at mga primaryang dokumento.