The Albanese government announced changes to the Petroleum Resource Rent Tax effective from 1 July 2023, specifically introducing a cap on deductions at 90% of PRRT assessable receipts for offshore LNG projects [1].

The $2.4 billion revenue increase figure is confirmed across government sources, stated as the projected increase "over the forward estimates" (typically 4-5 years from announcement) [1] [2].

This means that LNG operators will have a taxable profit floor of at least 10% of their assessable receipts, regardless of available deduction credits [3].

The cap applies to offshore LNG producers and includes additional measures responding to the Treasury Gas Transfer Pricing Review and the 2018 Callaghan PRRT Review [2].

This delay means major projects like Gorgon, Ichthys, and Prelude—which are 7+ years into production—face immediate application, while newer projects have prolonged exemptions [4].

Critically, even the gas industry—normally opposed to tax increases—supported these reforms, according to the Australia Institute, indicating the measure is insufficient to deliver "fairer" taxation [5].

# # # # # # 資源 nounShigen 富 nounTomi に direction/targetNi 対する verbTaisuru 課税 nounKazei が subject-markerGa 不 Fu 十分 Juu fun

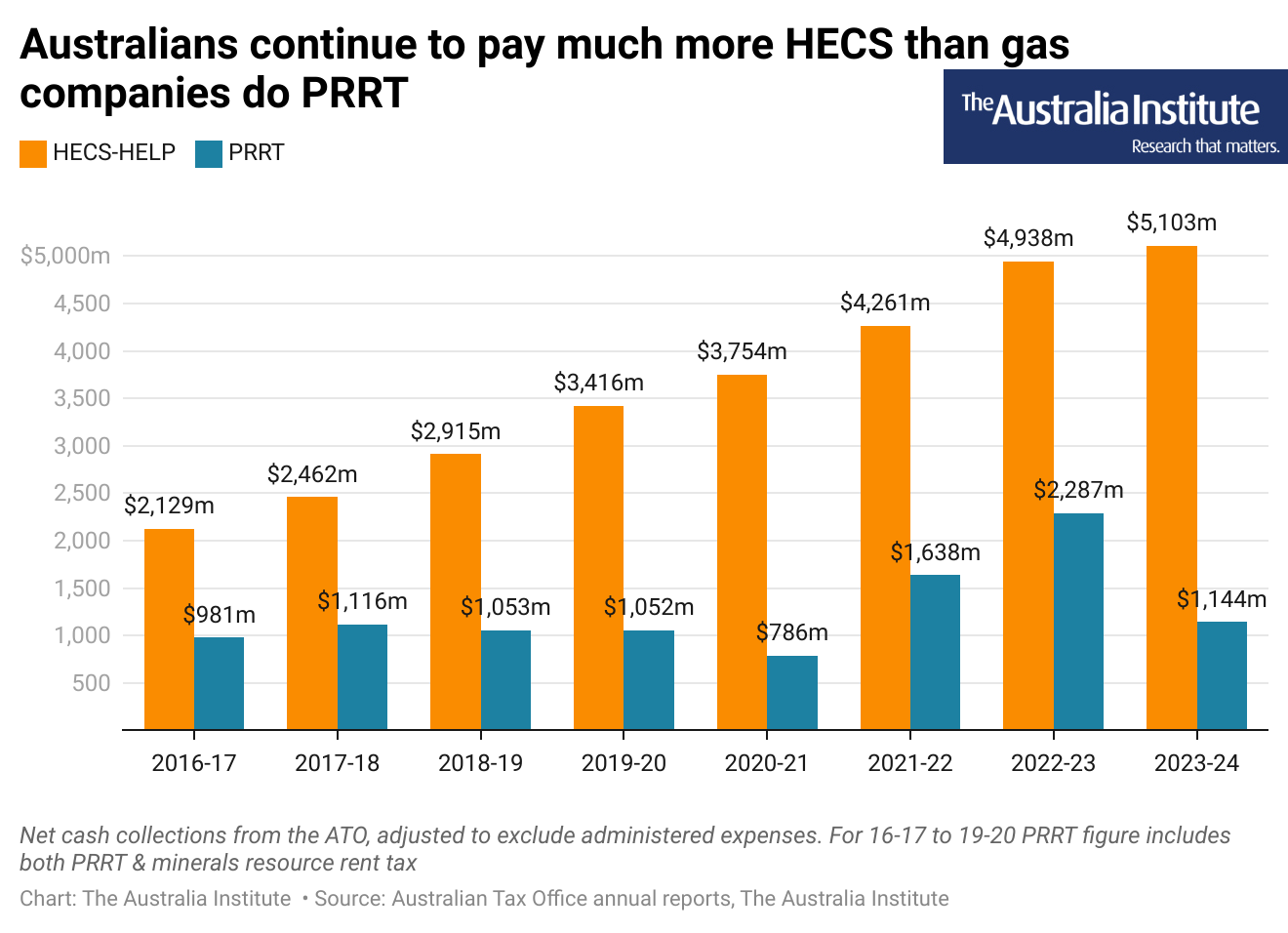

Data reveals the extent of the problem the $2.4 billion reform addresses: in 2023-24, Australians paid more than 4 times on HECS/HELP student loans than gas companies paid on PRRT [6].

The Australia Institute explicitly notes that the 90% cap "does little more than move some PRRT revenue forward and does not mean gas companies will be paying more PRRT over time" [5].

This is critical: the reform accelerates revenue collection from existing high-profit periods, but does not structurally increase the proportion of profits that are taxed.

The PRRT reform should be understood as a carefully calibrated political compromise that delivers genuine but limited revenue benefits while maintaining investor confidence [2].

The government balanced several competing interests: (1) extracting more revenue from profitable LNG projects, (2) maintaining investment certainty for energy security, (3) avoiding industry opposition, and (4) appearing to address "gas industry super profits" criticism.

Woodside Energy CEO James Tooley warned that "over-reaching" on tax reform could "undercut future revenue and hamper investment needed to boost supply," implying the government stayed comfortably within acceptable bounds from an industry perspective [4].

Chevron stated they did not believe changes to PRRT were necessary at all [4], yet proceeded without significant commercial impact—suggesting the cap is not particularly burdensome.

When experts argue that alternative deduction caps (80% or 60%) would raise 5-7x more revenue with similar economic effect, it indicates the government's chosen 90% level was a political decision, not an economic maximum [5].

However, presenting this as a comprehensive reform masks that:

1. **Better alternatives exist** - More aggressive caps would deliver 5-7x more revenue [5]

2. **Revenue is temporary** - Benefits frontloaded, diminish over time as high-profit periods end

3. **Tax rate remains low** - Even with reform, gas companies pay less tax than Australian students pay on loans [6]

4. **Structural problems persist** - Deduction-heavy model allows minimal long-term taxation regardless of commodity prices [5]

The government implemented the weakest politically viable version of PRRT reform—industry support for the measure indicates this—while failing to address structural problems that allow gas companies to pay minimal tax relative to resource wealth extracted.

Presenting this as "reformed PRRT" without acknowledging the existence of substantially stronger alternatives is strategically misleading about the government's commitment to ensuring fair resource taxation.

The government implemented the weakest politically viable version of PRRT reform—industry support for the measure indicates this—while failing to address structural problems that allow gas companies to pay minimal tax relative to resource wealth extracted.

Presenting this as "reformed PRRT" without acknowledging the existence of substantially stronger alternatives is strategically misleading about the government's commitment to ensuring fair resource taxation.