This is indeed the longest consecutive period of annual real wage growth in almost a decade, following a sequence of ten straight quarters of decline prior to this period [2].

However, this claim represents a deeply misleading framing of Australia's wage position:

1. **Still below pre-crisis levels**: The RBA explicitly states that "Real wages...have declined by around 5 per cent since 2021 and remain around their 2023 trough" [4].

Real wages remain substantially below 2019 levels [5].

2. **Cumulative loss unaddressed**: The OECD notes that "real wages...remain below 2019 levels in most" OECD countries [5].

Rather than celebrating recent growth, this reveals persistent wage stagnation and loss since 2019 - a permanent hit to workers' living standards.

3. **Modest growth rates obscured**: The government emphasizes the streak of consecutive quarters while downplaying that individual quarterly growth is very modest (typically 0.5-0.8% annually) [3].

These are small gains after a decade of near-zero growth.

4. **Cost of living crisis context**: While wages have begun growing faster than measured inflation, the broader cost of living - particularly housing, energy, and food - has grown much faster than wage growth and CPI would suggest [6].

Real living standards remain under pressure despite positive wage growth.

5. **Still not recovering cumulative loss**: Even with eight quarters of growth, workers are materially worse off than 2019.

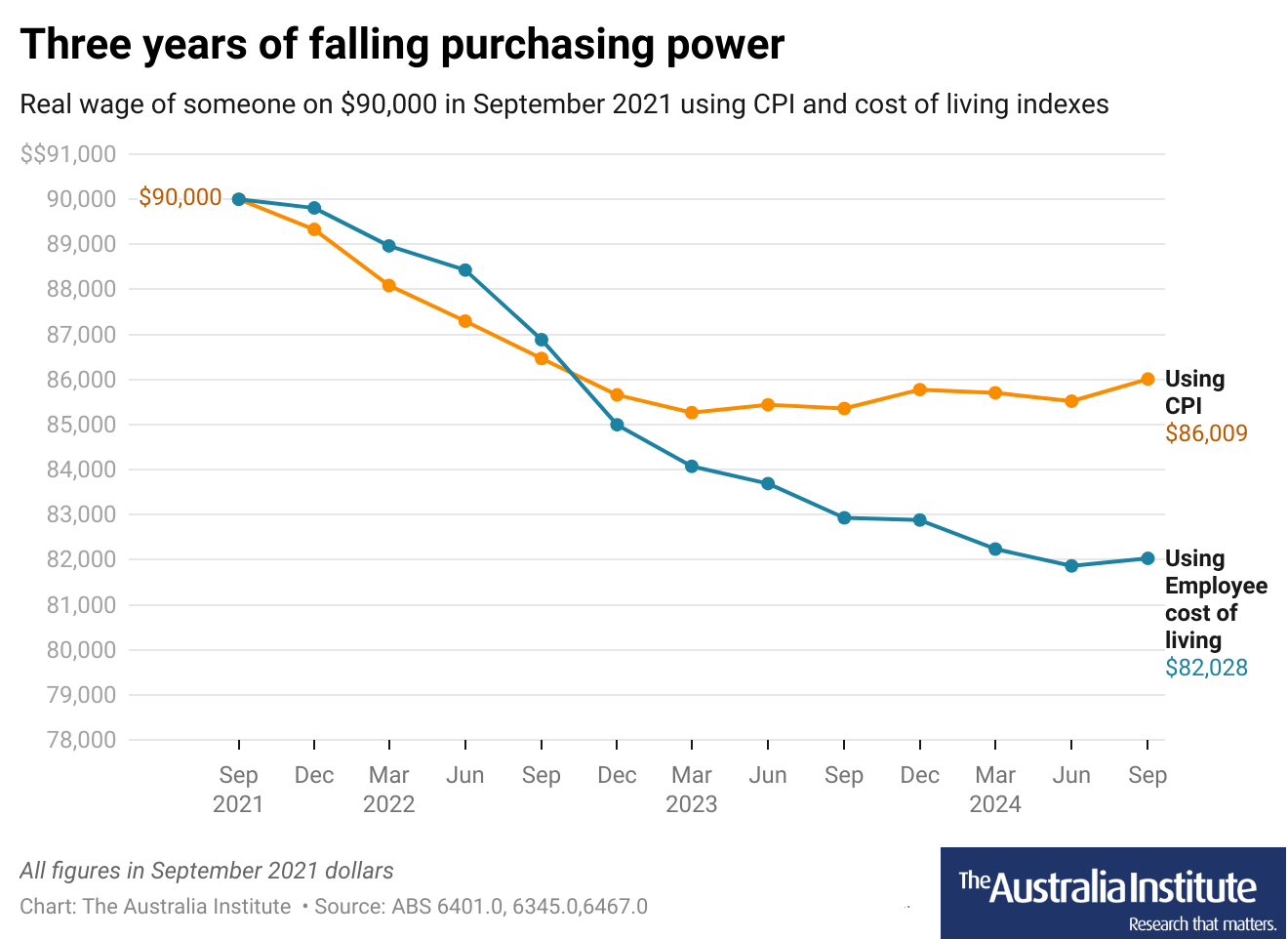

The Australia Institute analysis found that "workers are $8,000 worse off than 3 years ago" despite wages growing faster than inflation [6].

6. **Long-term stagnation admission**: The claim that this is the "longest run in almost a decade" is an admission of systemic wage stagnation.

It implicitly acknowledges a decade of wage crisis - this small positive streak is newsworthy precisely because wage growth has been absent for so long.

The claim is technically true but frames systemic failure as achievement:

1. **Celebrating recovery from self-inflicted damage**: The government is presenting recovery from inflation-driven real wage losses as an accomplishment.

By that measure, there is no achievement - wages have not recovered.

2. **Misleading timeframe selection**: Highlighting "longest run in almost a decade" while ignoring that this came after a decade of stagnation uses a misleading comparative frame.

A more honest statement: "After nearly a decade of wage stagnation and decline, real wages have begun modestly recovering" - which sounds very different.

3. **Hiding the broader cost-of-living crisis**: While nominal wages grew 3.4% and inflation measured 2.4%, the actual cost of living experienced by workers (housing, energy, groceries) rose faster [6].

The wage growth claim obscures this reality.

4. **Tiny gains framed as significant**: Annual real wage growth of 0.8-1.3% is presented as major achievement when it merely represents recovery toward pre-2019 levels [3].

True wage growth achievement would be wages exceeding 2019 levels, not recovering toward them.

5. **Short-term phenomenon unclear**: It remains unclear whether this growth will persist or represents a temporary cyclical improvement.

Real wages remain substantially below 2019 levels, workers are worse off than three years ago, and the growth streak represents recovery from recent lows, not achievement of new prosperity.

Real wages remain substantially below 2019 levels, workers are worse off than three years ago, and the growth streak represents recovery from recent lows, not achievement of new prosperity.