The Claim

“Reformed Petroleum Resource Rent Tax, increasing receipts by $2.4 billion”

Original Sources Provided

✅ FACTUAL VERIFICATION

The core claim about PRRT reform is factually accurate. The Albanese government announced changes to the Petroleum Resource Rent Tax effective from 1 July 2023, specifically introducing a cap on deductions at 90% of PRRT assessable receipts for offshore LNG projects [1]. The $2.4 billion revenue increase figure is confirmed across government sources, stated as the projected increase "over the forward estimates" (typically 4-5 years from announcement) [1] [2].

The centerpiece reform is the deductions cap: limiting the proportion of PRRT assessable income that can be offset by deductions to 90 per cent [1]. This means that LNG operators will have a taxable profit floor of at least 10% of their assessable receipts, regardless of available deduction credits [3]. The cap applies to offshore LNG producers and includes additional measures responding to the Treasury Gas Transfer Pricing Review and the 2018 Callaghan PRRT Review [2]. The government proceeded with eight of eleven recommendations from the GTP Review and eight recommendations from the Callaghan Review [2].

Missing Context

However, the claim critically omits significant context about the actual effectiveness and adequacy of the reforms.

Scope and Limitations

The deductions cap only begins applying after a project has been producing for 7 years, softening the impact on new developments [4]. This delay means major projects like Gorgon, Ichthys, and Prelude—which are 7+ years into production—face immediate application, while newer projects have prolonged exemptions [4].

Revenue Impact is Modest and Debated

The Australia Institute's analysis demonstrates the reforms raise substantially less revenue than more aggressive alternatives [5]. While the 90% cap raises $2.4 billion, an 80% cap would raise $13.42 billion over four years, and a 60% cap would raise $18.60 billion [5]. This indicates the government chose a deliberately weak version of PRRT reform. Critically, even the gas industry—normally opposed to tax increases—supported these reforms, according to the Australia Institute, indicating the measure is insufficient to deliver "fairer" taxation [5].

Insufficient Tax on Resource Wealth

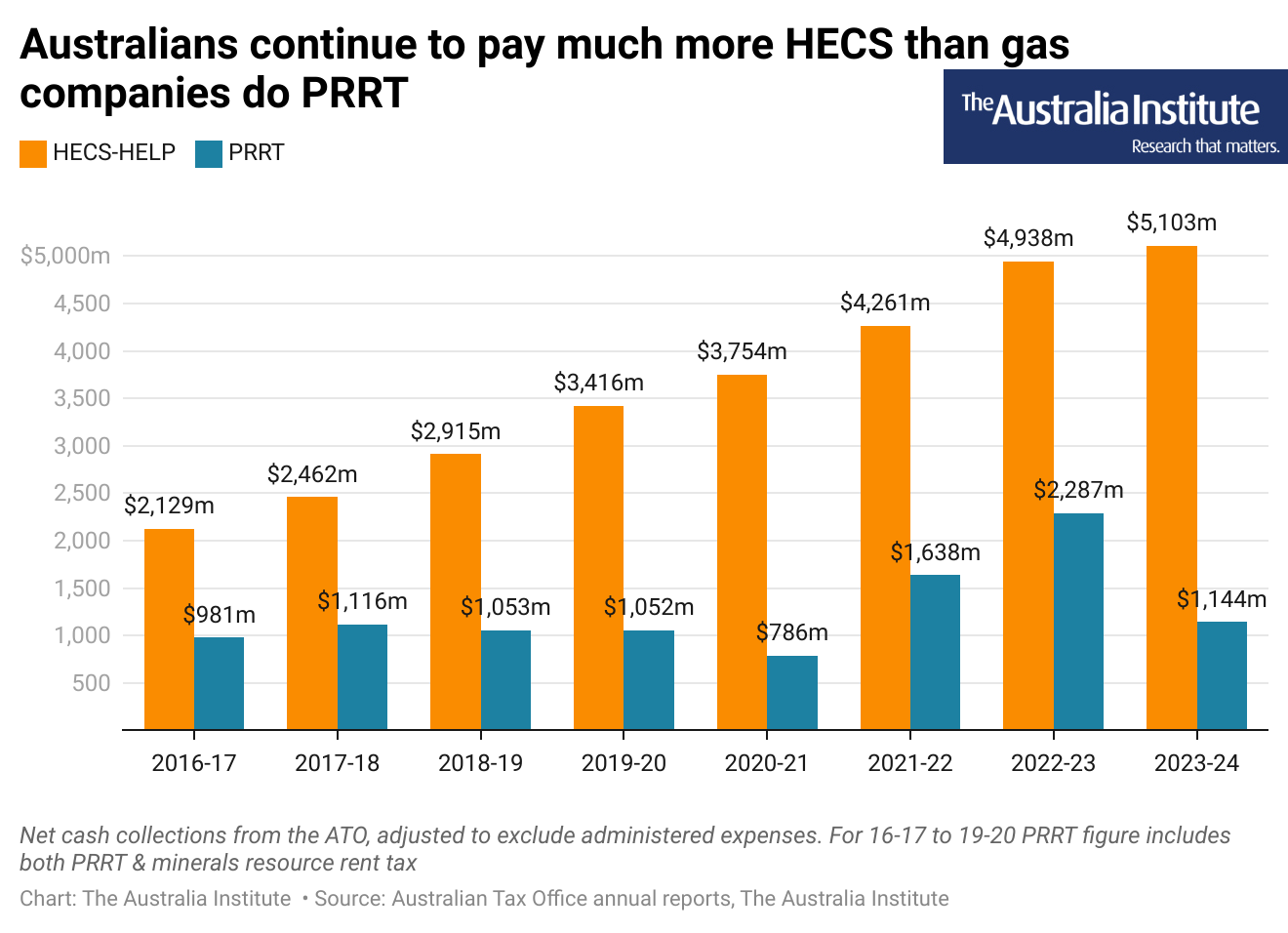

Data reveals the extent of the problem the $2.4 billion reform addresses: in 2023-24, Australians paid more than 4 times on HECS/HELP student loans than gas companies paid on PRRT [6]. This comparison illustrates that despite the reforms, gas companies' tax contribution remains minimal relative to resource wealth extracted. The PRRT itself is acknowledged by experts as a structurally weak tax that allows companies to offset most profits through deduction claims [5].

"Moving Forward" Rather Than Structural Change

The Australia Institute explicitly notes that the 90% cap "does little more than move some PRRT revenue forward and does not mean gas companies will be paying more PRRT over time" [5]. This is critical: the reform accelerates revenue collection from existing high-profit periods, but does not structurally increase the proportion of profits that are taxed. Once deduction credits are exhausted, companies revert to minimal PRRT obligations.

Temporary Nature of Benefits

The revenue increase is frontloaded. When commodity prices fall or projects move past their peak profit periods, the reform delivers diminishing returns. By the 2030s, when global LNG competition increases and prices moderate, the $2.4 billion benefit will likely diminish substantially [5].

💭 CRITICAL PERSPECTIVE

The PRRT reform should be understood as a carefully calibrated political compromise that delivers genuine but limited revenue benefits while maintaining investor confidence [2]. The government balanced several competing interests: (1) extracting more revenue from profitable LNG projects, (2) maintaining investment certainty for energy security, (3) avoiding industry opposition, and (4) appearing to address "gas industry super profits" criticism.

The evidence suggests the government chose the weaker end of that spectrum. The fact that the gas industry did not oppose these reforms indicates they viewed the measures as manageable. Woodside Energy CEO James Tooley warned that "over-reaching" on tax reform could "undercut future revenue and hamper investment needed to boost supply," implying the government stayed comfortably within acceptable bounds from an industry perspective [4]. Chevron stated they did not believe changes to PRRT were necessary at all [4], yet proceeded without significant commercial impact—suggesting the cap is not particularly burdensome.

When experts argue that alternative deduction caps (80% or 60%) would raise 5-7x more revenue with similar economic effect, it indicates the government's chosen 90% level was a political decision, not an economic maximum [5].

The $2.4 billion claim is factually accurate but strategically incomplete. The government should be credited for delivering real additional revenue and responding to public pressure on gas taxation. However, presenting this as a comprehensive reform masks that:

- Better alternatives exist - More aggressive caps would deliver 5-7x more revenue [5]

- Revenue is temporary - Benefits frontloaded, diminish over time as high-profit periods end

- Tax rate remains low - Even with reform, gas companies pay less tax than Australian students pay on loans [6]

- Structural problems persist - Deduction-heavy model allows minimal long-term taxation regardless of commodity prices [5]

PARTIALLY TRUE

6.5

out of 10

The $2.4 billion figure is factually accurate and the reform is genuine. However, the claim is misleading through context omission. The government implemented the weakest politically viable version of PRRT reform—industry support for the measure indicates this—while failing to address structural problems that allow gas companies to pay minimal tax relative to resource wealth extracted. Presenting this as "reformed PRRT" without acknowledging the existence of substantially stronger alternatives is strategically misleading about the government's commitment to ensuring fair resource taxation.

Final Score

6.5

OUT OF 10

PARTIALLY TRUE

The $2.4 billion figure is factually accurate and the reform is genuine. However, the claim is misleading through context omission. The government implemented the weakest politically viable version of PRRT reform—industry support for the measure indicates this—while failing to address structural problems that allow gas companies to pay minimal tax relative to resource wealth extracted. Presenting this as "reformed PRRT" without acknowledging the existence of substantially stronger alternatives is strategically misleading about the government's commitment to ensuring fair resource taxation.

📚 SOURCES & CITATIONS (6)

-

1

Implementing reforms to the Petroleum Resource Rent Tax

The Albanese Government is reforming the Petroleum Resource Rent Tax (PRRT) to deliver a fairer return to the Australian community from their natural resources.

Ministers Treasury Gov -

2

Changes to the Petroleum Resource Rent Tax

The Albanese Government will introduce changes to the Petroleum Resource Rent Tax (PRRT) to deliver a fairer return to the Australian community from their natural resources.

Ministers Treasury Gov -

3

PRRT deductions cap

Ato Gov

-

4

What Australia's new gas tax will mean for new projects, the economy and the climate

Changes to the petroleum resource rent tax (PRRT) are long overdue, but Labor’s modest attempt at reform represents a missed opportunity.

The Conversation -

5PDF

A stronger PRRT cap A fairer way to tax gas super profits

Australiainstitute Org • PDF Document -

6

In 2023-24 Australians paid more than 4 times on HECS/HELP than gas companies did on PRRT

In 2023-24 tax from the PRRT was less than an quarter the amount raised by HECS/HELP debts repayments.

The Australia Institute

Rating Scale Methodology

1-3: FALSE

Factually incorrect or malicious fabrication.

4-6: PARTIAL

Some truth but context is missing or skewed.

7-9: MOSTLY TRUE

Minor technicalities or phrasing issues.

10: ACCURATE

Perfectly verified and contextually fair.

Methodology: Ratings are determined through cross-referencing official government records, independent fact-checking organizations, and primary source documents.